Why would you do an interest-only mortgage?

Interest-only mortgages can be appropriate for borrowers who are disciplined enough to make periodic principal payments as well. They might also work for someone with a job that pays large annual bonuses that can be used to pay down the principal balance of the loan each year.

What happens with an interest-only mortgage?

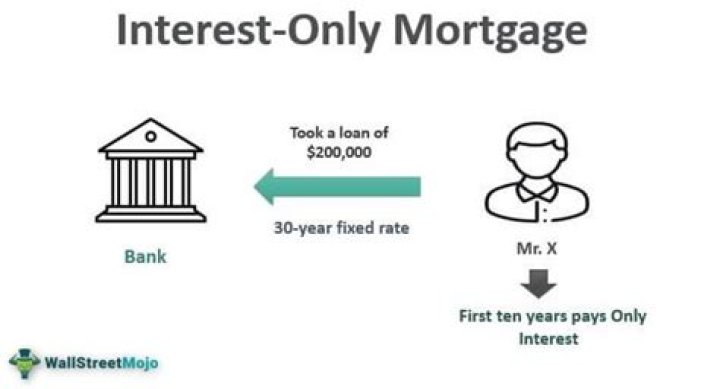

With an interest-only mortgage, your monthly payment pays only the interest charges on your loan, not any of the original capital borrowed. This means your payments will be less than on a repayment mortgage, but at the end of the term you’ll still owe the original amount you borrowed from the lender.

How long can you get interest-only mortgage?

Interest-only mortgages will come with an initial rate, often lasting between two and 10 years. After this, if you don’t remortgage, you’ll be put onto the lender’s standard variable rate, which is likely to be uncompetitive.

What does it mean to have interest only mortgage?

What is an interest-only mortgage? An interest-only mortgage is a loan which requires the borrower to pay the interest charged on the loan, and not the amount borrowed. The borrower only repays the loan when the term finishes.

How long does an interest only loan last?

How an interest-only mortgage works An interest-only loan is offered for a relatively short term, usually five to 10 years. If you remain in the home, you can refinance the loan into a traditional principal-and-interest mortgage, or sign up for another interest-only term.

Which is better interest only or fixed rate mortgage?

If you want a monthly payment on your mortgage that’s lower than what you can get on a fixed-rate loan, you might be enticed by an interest-only mortgage. By not making principal payments for several years at the beginning of your loan term, you’ll have better monthly cash flow. But what happens when the interest-only period is up?

Can you make principal payments on an interest only mortgage?

If you want to make principal payments during the interest-only period, you can, but that’s not a requirement of the loan. You’ll usually see interest-only loans structured as 3/1, 5/1, 7/1 or 10/1 adjustable-rate mortgages (ARMs).