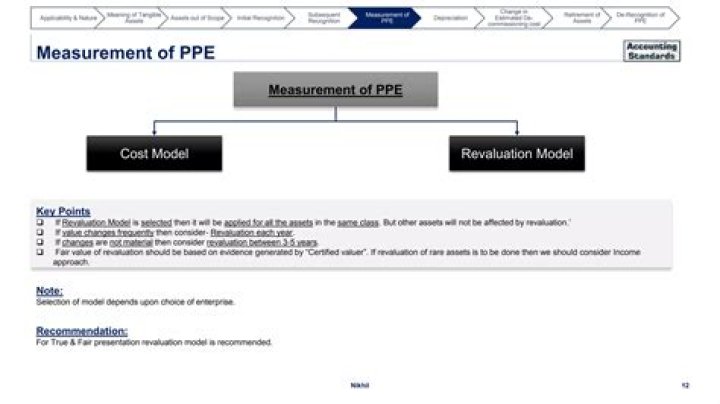

Why would a business use the revaluation model to measure PPE?

The revaluation model gives a business the option of carrying a fixed asset at its revalued amount. Under this approach, one must continue to revalue fixed assets at sufficiently regular intervals to ensure that the carrying amount does not differ materially from the fair value in any period.

Why is revaluation model better than cost model?

According to this method, the non-current asset is carried at a revalued amount less depreciation. The principal reason for companies to adopt this approach is to ensure that noncurrent assets are shown at their market value in financial statements, thus this provides a more accurate picture than the cost model.

What is the basis of revaluation of PPE?

When an item of PPE is revalued, there are two methods of dealing with accumulated depreciation with the most commonly used method being the following whereby; Accumulated depreciation is eliminated against the gross carrying value of the asset and the net amount restated to the revalued amount of the asset.

What is difference between cost model and revaluation model?

Under cost model, the asset is carried at its cost less accumulated depreciation less impartment loss and under revaluation model, if fair value can be measured reliably; revalued amount is equal to Fair value at revaluation date minus any subsequent accumulated depreciation & impairment losses.

What is the difference between revaluation model and cost model?

What is the difference between revaluation model and fair value model?

Any changes in the fair value are posted in profit and loss account. The revaluation model is however different as the organisation may not need to revalue the asset every reporting period but should be done with sufficient regularity to ensure the account balance isn’t too far off the fair value.

How do you account for revaluation of PPE?

PPE is carried at its historical cost minus any accumulated depreciation and impairment loss since its recognition. PPE is carried at its fair value (at the date of the revaluation) less any subsequent accumulated depreciation and impairment loss.

What is revaluation value?

Revaluation is an adjustment made to the recorded value of an asset to accurately reflect its current market value. When purchasing a fixed asset, it is usually recorded at cost-price.

Can I change from cost model to revaluation model?

Yes, You can change the machinery from cost model to revaluation model and move the asset from carrying value to fair value less accumulated depreciation and impairment. Moreover, the fair value must be measured reliably and there is no substantial difference between carrying value and fair value.

Can we change from revaluation model to cost model?

Changing from the revaluation to the cost model where reliable fair valuations are available or determinable. Another common error occurs when an entity changes it measurement model (accounting policy) for a class of assets from the cost basis to the revaluation basis.

How do you use the revaluation method?

Under revaluation method a competent person values the asset concerned at the end of each financial year and the depreciation is calculated by deducting the value at the end of the year from the value at the beginning of the year.

Can I change from revaluation model to cost model?

Why do companies choose cost models?

Companies avoid the use the fair value model to neglect the reporting of revaluation gain arising from asset valuation, increasing the company’s size. Instead, companies will choose the cost model in order to reduce the political burden a company has to bear (Quagli & Avallone, 2010).

Why do most companies use the cost model instead of the revaluation model to account for property plant and equipment?

The principal reason for companies to adopt this approach is to ensure that noncurrent assets are shown at their market value in financial statements, thus this provides a more accurate picture than the cost model. However, this is a costly exercise since revaluation should be carried out at regular intervals.

What is the difference between fair value and revaluation?

other than fair value model don’t have depreciation whereas revaluation model have depreciation. If there is a gain in the fair value model for Investment property, is it the gain is also called it as gain on revaluation which is the same for revaluation model for ppe???

What is revaluation method?

A method of determining the depreciation charge on a fixed asset against profits for an accounting period. The asset to be depreciated is revalued each year; the fall in the value is the amount of depreciation to be written off the asset and charged against the profit and loss account for the period.

How is revaluation calculated?

What do revaluation means?

A revaluation is a calculated upward adjustment to a country’s official exchange rate relative to a chosen baseline. Revaluation is the opposite of devaluation, which is a downward adjustment of a country’s official exchange rate.

How does the revaluation model work for a business?

The revaluation model. The revaluation model gives a business the option of carrying a fixed asset at its revalued amount. Subsequent to the revaluation, the amount carried on the books is the asset’s fair value, less subsequent accumulated depreciation and accumulated impairment losses.

When to use the revaluation model in IAS 16?

The carrying value is also adjusted for any re-measurement of the lease liability. If an entity applies the revaluation model under IAS 16 to any class of property, plant or equipment then a lessee MAY elect to apply the revaluation model to right-of-use assets of the same class

How are impairment losses treated in the revaluation model?

Please note that impairment loss can be noted by either crediting the relevant PPE account or the accumulated impairment losses account. The revaluation model allows restoration of impairment losses, but how it should be treated depends on whether or not gain on revaluation exceeds their amount.

How are revaluation models used in IFRS accounting?

IFRS regulates accounting for property, plant, and equipment (PPE) on the basis of IAS 16. Any entity can set up either a cost model or a revaluation model as an accounting policy, applying it to the entire class of Property, Plant, and Equipment.