Why is an ARM loan a bad idea?

With an ARM, you’ll never be able to fully know how much you’ll be paying each month and how much your home will ultimately cost you in the long run. How crazy is that? That’s why ARMs are bad news—and why some mortgage lenders intentionally make understanding them so complicated!

What are the advantages of an ARM mortgage?

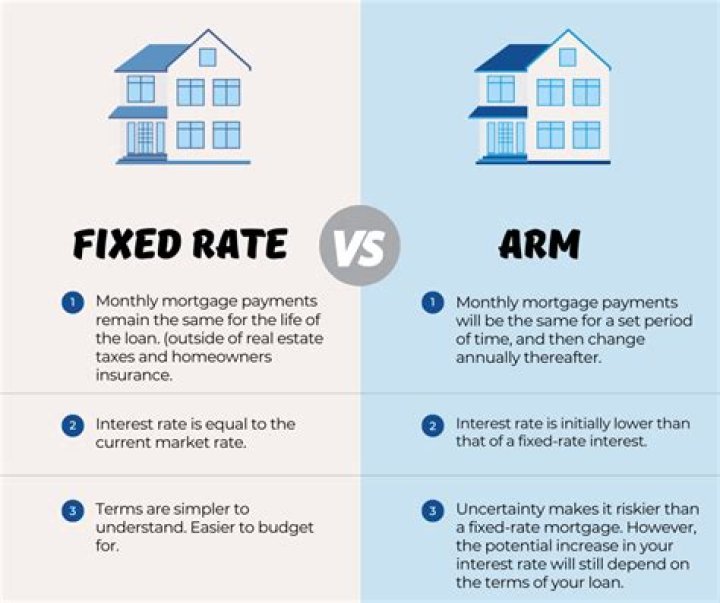

Pros of an adjustable-rate mortgage It has lower rates and payments early in the loan term. Because lenders can consider the lower payment when qualifying borrowers, people can buy more expensive homes than they otherwise could. It allows borrowers to take advantage of falling rates without refinancing.

What is an ARM mortgage?

Adjustable-rate mortgage (ARM) A mortgage that does not have a fixed interest rate. The rate changes during the life of the loan based on movements in an index rate, such as the rate for Treasury securities or the Cost of Funds Index. ARMs usually offer a lower initial interest rate than fixed-rate loans.

What is a disadvantage of an ARM adjustable-rate mortgage )?

ARMs require borrowers to plan for when the interest rate starts changing and monthly payments may grow. Even with careful planning, though, you might be unable to sell or refinance when you want to. If you can’t make the payments after the fixed-rate phase of the loan, you could lose the home.

Which is better an arm or fixed rate mortgage?

The initial interest rate for an ARM is lower than that of a fixed rate mortgage, where the interest rate remains the same during the life of the loan. A lower rate means lower payments, which might help you qualify for a larger loan.

Which is riskier an arm or a jumbo mortgage?

ARMs become even riskier with jumbo mortgages because the higher your principal, the more a change in interest rate is going to affect your monthly payment. Keep in mind, though, that adjustable interest rates don’t just rise.

Is there a lifetime limit on an arm mortgage?

Loans that qualify applicants based on artificially-low rates are no longer allowed. And the most popular ARM mortgage — the hybrid with introductory rates that can be fixed for three to ten years — is backstopped with caps in rate increases and lifetime limits to keep loans affordable. Borrowers can choose from 3/1,…

Which is an example of an ARM loan?

One common example is the 2/28 ARM. The 2/28 ARM is a 30-year mortgage with a fixed interest rate for two years before being adjusted. Another typical version of the ARM loan, the 3/27 ARM, has a fixed interest rate for three years before it becomes variable. In these types of loans, the floating rate is determined based on an index plus a margin.