Why a reverse mortgage is a bad idea?

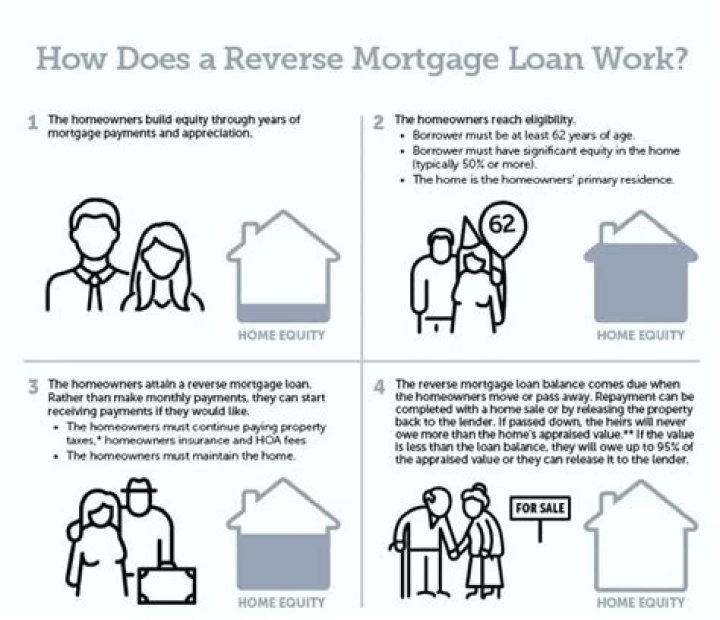

Reverse mortgage proceeds may not be enough to cover property taxes, homeowner insurance premiums, and home maintenance costs. Failure to stay current in any of these areas may cause lenders to call the reverse mortgage due, potentially resulting in the loss of one’s home.

What is the end result of a reverse mortgage?

When a reverse mortgage borrower dies, a lender will typically explain options for paying off the loan to the borrower’s estate. Heirs then have 30 days to decide what to do. If heirs decide to pay off the HECM, they have six months to sell the property or pay off the HECM, possibly with a new mortgage.

How does a reverse mortgage work for You?

A reverse mortgage is a loan based on the paid-up current value, or equity, in your home. Unlike a conventional mortgage, your lender pays you — in monthly payments, through a variable line of credit or in a lump sum. You don’t have to repay the loan until you sell your house, move or die.

What are the pros and cons of reverse mortgage in Canada?

The Pros and Cons of Reverse Mortgages in Canada. A reverse mortgage is a mortgage product that allows senior homeowners (55+) to borrow up to 50% of the value of their home. A reverse mortgage is secured by the equity in your home and, unlike a home equity line of credit (HELOC), it does not require any income proof verification.

What happens if you default on a reverse mortgage?

Reverse mortgage underwriting guidelines require that the borrower maintain property charges and occupy their home as a primary residence. If you fail to do so, the loan servicer must call the loan do and payable and force the borrower to either refinance or sell the home.

How can I find out if my reverse mortgage is accurate?

It’s a good idea to check with your reverse mortgage servicer to make sure its loan records are accurate and that you and your co-borrower are both on the loan. Call your servicer to find out what names are listed on your loan.