Who funds the life and Health Insurance guaranty association?

The guaranty association’s coverage of insurance company insolvencies is funded by post-insolvency assessments of the other guaranty association member companies.

What is the most the insurance guaranty association will pay?

Insurance guaranty associations are given their powers by the state insurance commissioner. Most of these organizations are funded with the money they collect from conducting assessments of member insurers. The total payout in most states is capped at $300,000 per individual.

Which insurer is eligible for state guaranty fund?

State guaranty funds guarantee payment for insurance policyholders should the insurance company default. The fund only covers beneficiaries of insurance companies where the insurer is licensed to sell products in that state.

Are annuities backed by the state?

Insurance companies, which issue annuities, are legally required to belong to their particular state’s guaranty association. Each state, as well as the District of Columbia and Puerto Rico, has a guaranty association, and every insurance company must belong to the guaranty association in the state where they operate.

How do you make money on life insurance?

“The most common ways people take money out of policies are: taking a loan from the policy, converting the cash value to an annuity [a series of regular payments], surrendering the policy, or leveraging riders such as enhanced long-term care benefits.”

Why are state life and health insurance guaranty associations important?

State life and health insurance guaranty associations provide a safety net for their state’s policyholders, ensuring that they continue to receive coverage even if their insurer is declared insolvent.

How much can a state guaranty association cover?

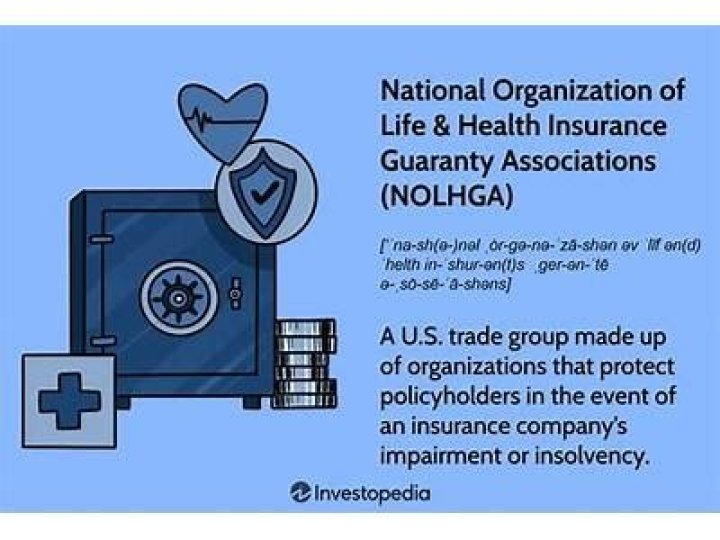

Some states cover more, as much as $1 million in the case of New York, according to the National Organization of Life & Health Insurance Guaranty Associations, an organization created to coordinate the 50 individual state guaranty funds. The coverage amounts are specified by a model law created by National Association of Insurance Commissioners.

Are there any state guaranty associations for annuities?

That’s not the case with annuities, which are legally considered insurance products issued by insurance companies rather than banks. But that doesn’t mean customers are without protection. Instead of federal protection, individual states provide the protection similar to the FDIC.

When was the NOLHGA insurance guaranty association founded?

NOLHGA was founded in 1983 when the state guaranty associations determined that there was a need for a mechanism to help them coordinate their efforts to provide protection to policyholders when a life or health insurance company insolvency affects people in many states.