Which function you will use to calculate payment for a loan?

Excel PMT function

The Excel PMT function is a financial function that returns the periodic payment for a loan. You can use the PMT function to figure out payments for a loan, given the loan amount, number of periods, and interest rate.

How do I calculate a loan payment in Excel?

=PMT(17%/12,2*12,5400)

- The rate argument is the interest rate per period for the loan. For example, in this formula the 17% annual interest rate is divided by 12, the number of months in a year.

- The NPER argument of 2*12 is the total number of payment periods for the loan.

- The PV or present value argument is 5400.

How to convert constant interest rate into monthly payments?

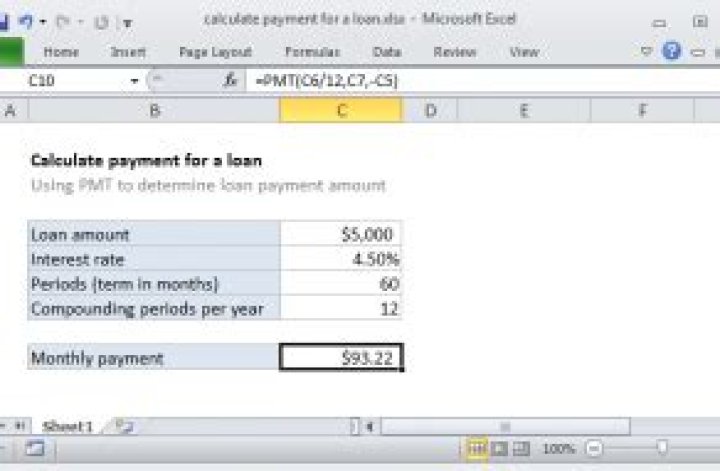

As the constant interest rate is annual, so we have to convert it into monthly interest rate by dividing it to 12 (compounding periods per year). The loan period is 5 years and payments for the loan are monthly, therefore the total number of payments would be 60 (12*5).

How to calculate the interest on a loan?

For a loan, you may also want to calculate other figures, such as how much you will pay in interest during the life of the loan, or in each periodic payment, how much portion is of interest. Such metrics can be calculating using the following functions:

Which is the function of PMT in a loan?

In the previous post, we learnt about the PMT function, which calculates the payment for a loan based on constant payments and a constant interest rate. For a loan, you may also want to calculate other figures, such as how much you will pay in interest during the life of the loan, or in each periodic payment, how much portion is of interest.

How to calculate the monthly payment for a loan?

The Syntax of the Formula Assume we need to borrow $30,000 at 8% annual interest rate for 5 years on monthly payment terms. We can calculate the monthly payment for this loan amount using the following formula assuming the monthly payment is due at the end of the month; Figure 3.