When the insured selects the extended term Nonforfeiture option?

If you chose the extended term nonforfeiture, then your accumulated cash value would purchase an extended term insurance policy with a term of 30 years and death benefit equal to the original insurance plan.

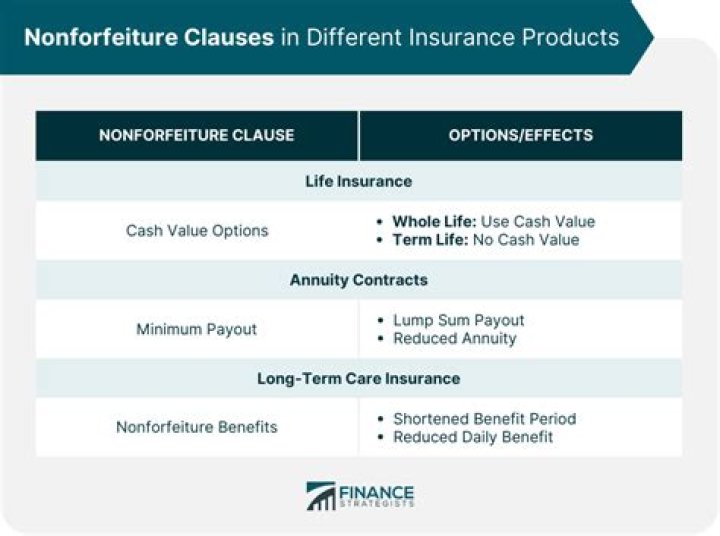

What is a Nonforfeiture benefit?

Nonforfeiture: A Nonforfeiture Benefit must be offered with Long Term Care Insurance policies. The nonforfeiture benefit is designed to ensure that if you lapse your policy (i.e., stop paying premiums) after a specified number of years, you retain some benefits from the policy.

What limits the amount that a policyowner may borrow from a whole life insurance policy a?

What limits the amount that a policyowner may borrow from a whole life insurance policy? Cash value – The amount available to the policyowner for a loan is the policy’s cash value. If there are any outstanding loans, that amount will be reduced by the amount of the unpaid loans and interest.

When a reduced paid up Nonforfeiture option is chosen what happens to the face amount?

a) The insurer may terminate the contract only at renewal for certain conditions. until the insured reaches age 65. When a reduced-paid up nonforfeiture option is chosen, what happens to the face amount of the policy? a) It is reduced to the amount of what the cash value would buy as a single premium.

What is Nonforfeiture interest rate?

Generally, an annuity repays the capital invested by a person over a set period of time plus interest. The minimum nonforfeiture rate, which is the minimum interest rate guarantee that an insurance company can use in an individual fixed annuity contract to determine its cash value, is regulated by the Insurance Code.

What are the three Nonforfeiture options?

There are three nonforfeiture options: (1) cash surrender; (2) reduced paid- up insurance; and (3) extended term insurance. If a policyowner chooses, he/she may request a cash payment of the cash values when the policy is surrendered.

When a reduced paid up Nonforfeiture option is chosen what happened to the face amount?

Is there a default non forfeiture option for extended term insurance?

Extended-term insurance allows a policyholder to quit paying the premiums but not forfeit the equity of their policy. The amount of cash value you will have built-in your policy will be reduced by the amount of any loans against it. Extended-term insurance is often the default non-forfeiture option.

What are the different types of life insurance nonforfeiture clauses?

Life insurance policyholders can select one of four nonforfeiture benefit options: the cash surrender value, extended term insurance, loan value, and paid-up insurance.

What’s the difference between term and extended term insurance?

The amount of cash value you will have built in your policy will be reduced by the amount of any loans against it. Extended term insurance is often the default non-forfeiture option. With extended term insurance, the face amount of the policy stays the same, but it is flipped to an extended term insurance policy.

What can you do with the cash value of a nonforfeiture clause?

Before issuing payment to the policy owner, outstanding loan amounts are satisfied with the cash value. Select companies offer an annuity option in the nonforfeiture clause, as well. The remaining cash value may be used to purchase an annuity free of commissions or expenses.