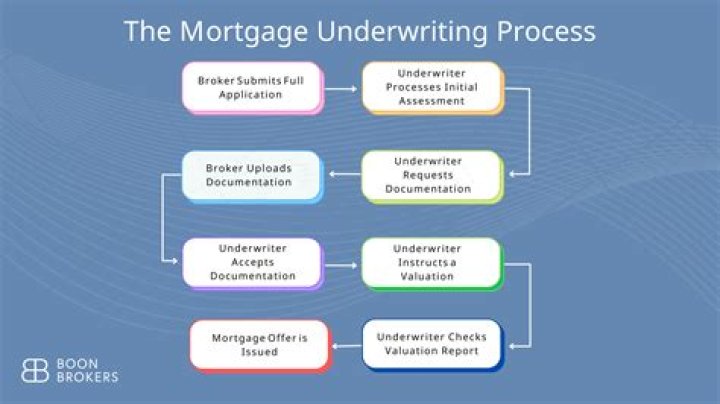

What is the underwriting part of a mortgage?

Mortgage underwriting is what happens behind the scenes once you submit your application. It’s the process a lender uses to take an in-depth look at your credit and financial background to determine if you’re eligible for a loan.

What would cause an underwriter to deny FHA mortgage?

Reasons for an FHA Rejection There are three popular reasons you have been denied for an FHA loan–bad credit, high debt-to-income ratio, and overall insufficient money to cover the down payment and closing costs.

How does the underwriting process for a mortgage work?

The mortgage underwriting process determines whether your finances are strong enough to repay the home loan you’re applying for. And, because anyone’s finances could take a turn for the worse, the underwriting process also evaluates whether the property you want to buy will be valuable enough to repay the loan if the lender has to foreclose.

What are the benefits of in house underwriting?

In-house underwriting enables mortgage consultants and underwriters to communicate more effectively on the details of your mortgage application and that can make all the difference in getting approved for a mortgage. Benefits of in-house underwriting. The biggest advantage is that borrowers have a more personal connection to the process.

Who is the underwriter for a home loan?

Here are the details: Your loan underwriter is ultimately the person who decides whether or not you can qualify for a mortgage. Your underwriter knows if you’re a good candidate just from looking into how you’ve handled money in the past.

Is it better to out source mortgage underwriting?

By contrast, many large mortgage lenders out-source the underwriting to third-party companies or individuals. This can save the lender a few dollars over-time but can also slow the process, introduce unnecessary costs for the borrower, and possibly create confusion with so many different hands on your loan file.