What is the default rate on reverse mortgages?

Default rates on HECMs have risen sharply — to between 8 and 10 percent in the years since the crisis —calling into question the viability of both the program and the Mutual Mortgage Insurance Fund.

What are the tax implications of a reverse mortgage?

No, reverse mortgage payments aren’t taxable. Reverse mortgage payments are considered loan proceeds and not income. The lender pays you, the borrower, loan proceeds (in a lump sum, a monthly advance, a line of credit, or a combination of all three) while you continue to live in your home.

What are the costs of a reverse mortgage?

There are several reverse mortgage costs, that could include, but are not limited to: Loan origination fee up to $6,000; An upfront mortgage insurance premium, which costs 2% of your home’s value; An annual mortgage insurance premium, which costs 0.5% of your home’s value A reverse mortgage counseling fee, which could cost $125 or more

What’s the principal limit on a reverse mortgage?

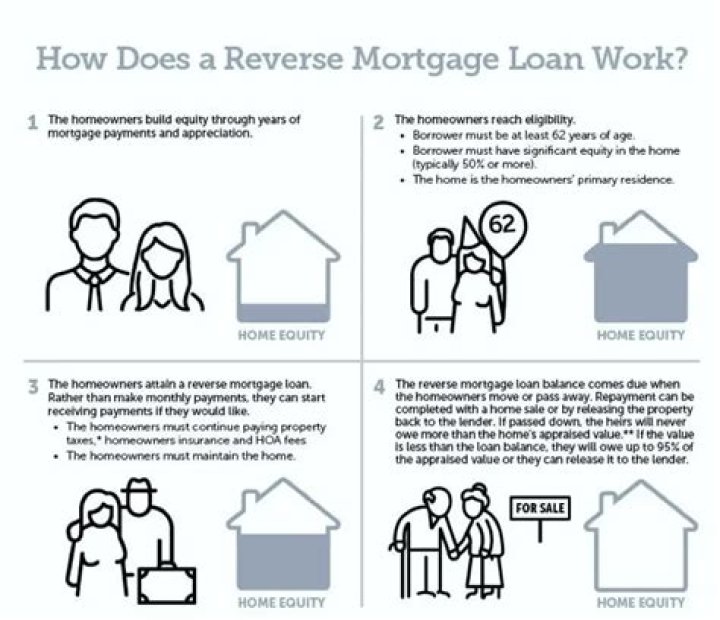

If you are married or co-borrowing with another person, the principal limit is based on the age of the youngest co-borrower, or Eligible Non-Borrowing Spouse. Lower cost than a lump sum payment because you’ll only be paying interest and fees on the money you use.

How old do you have to be to get reverse mortgage?

The most common reverse mortgage taken by consumers is a Home Equity Conversion Mortgage (HECM). It’s a type of home loan exclusively provided for homeowners aged 62 years old and above. HECMs are federally insured reverse mortgages that are backed by the U.S. Department of Housing and Urban Development ( HUD ).

Is the interest on a reverse mortgage tax deductible?

Interest on reverse mortgages is not deductible on income tax returns – until the loan is paid off, either partially or in full. You have to pay other costs related to your home. In a reverse mortgage, you keep the title to your home. That means you are responsible for property taxes, insurance, utilities, fuel,…