What is the 28 36 mortgage rule?

A Critical Number For Homebuyers

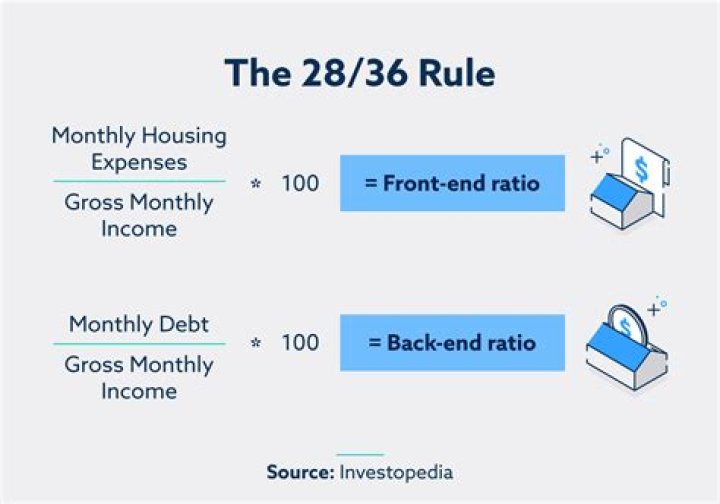

One way to decide how much of your income should go toward your mortgage is to use the 28/36 rule. According to this rule, your mortgage payment shouldn't be more than 28% of your monthly pre-tax income and 36% of your total debt. This is also known as the debt-to-income (DTI) ratio.What is the 35 45 rule?

With the 35% / 45% model, your total monthly debt, including your mortgage payment, shouldn't be more than 35% of your pre-tax income, or 45% more than your after-tax income. To calculate how much you can afford with this model, determine your gross income before taxes and multiply it by 35%.What is the ideal mortgage ratio to income?

Most lenders recommend that your DTI not exceed 43% of your gross income. 3 To calculate your maximum monthly debt based on this ratio, multiply your gross income by 0.43 and divide by 12.Does 28 36 Rule include taxes?

Front-end ratio: No more than 28% of your incomeThe front-end ratio is how much of your income is taken up by your housing expenses. According to the 28/36 rule, your mortgage payment -- including taxes, homeowners insurance, and private mortgage insurance -- shouldn't go over 28%.

How many times your income should your house be?

The total house value should generally be no more than 3 to 5 times your total household income, depending on how much debt you currently have. If you are completely debt-free, congratulations—you can consider houses that are up to 5 times your total household income.Use the 28/36 rule to find out how much house you can afford by Chris Menard

What is the 50 20 30 budget rule?

The rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must-have or must-do. The remaining half should be split up between 20% savings and debt repayment and 30% to everything else that you might want.How many times your salary do you need to retire?

According to these parameters, you may need 10 to 12 times your current annual salary saved by the time you retire. Experts say to have at least seven times your salary saved at age 55. That means if you make $55,000 a year, you should have at least $385,000 saved for retirement.How much debt is acceptable for a mortgage?

Most lenders will lend below 100% debt-to-income ratio. 50% is a common limit, but some lenders are more cautious. At the time of writing, only one lender does not lend to applicants with a debt-to-income ratio above 25%.How is 28 rule calculated?

The first part of the rule states that the maximum household expenses or housing costs should not be higher than 28 percent of your monthly income. Maximum household expenses typically include principal, interest, taxes and insurance.What percentage of your income should your mortgage be Dave Ramsey?

How Much House Can I Afford Based on My Salary? To calculate how much house you can afford, use the 25% rule—never spend more than 25% of your monthly take-home pay (after tax) on monthly mortgage payments.Can I buy a house if I make 45000 a year?

It's definitely possible to buy a house on a $50K salary. For many borrowers, low-down-payment loans and down payment assistance programs are putting homeownership within reach. But everyone's budget is different. Even people who make the same annual salary can have different price ranges when they shop for a new home.Do lenders look at gross or net income?

When determining how your debt relates to your income, lenders use your gross monthly income, not your net monthly income. Net monthly income is your monthly income after all taxes, Social Security payments and deductions for retirement accounts are taken out of your paycheck.How much income do I need for a 500K mortgage?

The Income Needed To Qualify for A $500k MortgageA good rule of thumb is that the maximum cost of your house should be no more than 2.5 to 3 times your total annual income. This means that if you wanted to purchase a $500K home or qualify for a $500K mortgage, your minimum salary should fall between $165K and $200K.

Is rent included in debt-to-income ratio?

*Remember your current rent payment or mortgage is not actually included in your DTI calculated by the lender.How much mortgage is too much?

Financial advisers and real estate professionals recommend that homeowners spend no more than 30 percent of their monthly income on their mortgage payment.What bills are included in debt-to-income ratio?

What monthly payments are included in debt-to-income?

- Monthly mortgage payments (or rent)

- Monthly expense for real estate taxes (if Escrowed)

- Monthly expense for home owner's insurance (if Escrowed)

- Monthly car payments.

- Monthly student loan payments.

- Minimum monthly credit card payments.

- Monthly time share payments.

Does having multiple credit cards affect mortgage?

Opening multiple card accounts in a short period of time can actually hurt your credit score and can also jeopardize larger financial goals like getting a low mortgage rate when buying a house.How can I lower my debt-to-income ratio quickly?

How to lower your debt-to-income ratio

- Increase the amount you pay monthly toward your debt. Extra payments can help lower your overall debt more quickly.

- Avoid taking on more debt. ...

- Postpone large purchases so you're using less credit. ...

- Recalculate your debt-to-income ratio monthly to see if you're making progress.