What is a tax imposed by the government on goods imported from another country?

A tariff is a tax imposed by one country on the goods and services imported from another country.

What is a tax imposed on imports to protect domestic industries from foreign competition called?

In simplest terms, a tariff is a tax. It adds to the cost borne by consumers of imported goods and is one of several trade policies that a country can enact. Tariffs are paid to the customs authority of the country imposing the tariff.

What is an example of tariff?

A tariff, simply put, is a tax levied on an imported good. There are two types. A “unit” or specific tariff is a tax levied as a fixed charge for each unit of a good that is imported – for instance $300 per ton of imported steel. An example is a 20 percent tariff on imported automobiles.

What is a tax that governments use to control international trade?

A tariff, at the most basic level, is a tax charged on goods or services as they move from one country to another. You may also see them referred to as a “customs duty,” as the term is often used interchangeably with “tariff.” Tariffs are typically charged by the country importing the goods.

What is a real world example of a tariff?

An example of a tariff could be a tariff on steel. This means that any steel imported from another country would incur a tariff, for example, 5% of the value of the imported goods, paid by the individual or business importing the goods.

Are tariffs good or bad for the economy?

Tariffs can have unintended side effects. They can make domestic industries less efficient and innovative by reducing competition. They can hurt domestic consumers since a lack of competition tends to push up prices.

What is the impact of tariffs on the economy?

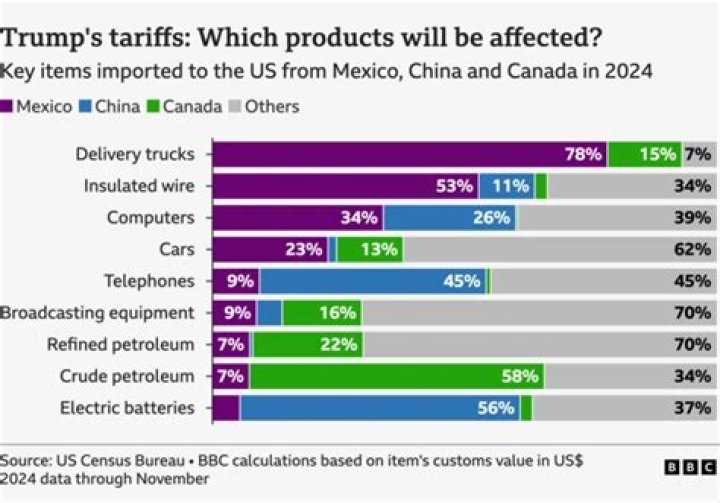

Tariffs affecting U.S. agricultural exports, 2018–19. All other things being equal, when foreign countries impose tariffs on exports of U.S. goods, the increased costs of these goods usually result in lower demand in the importing country, creating a supply surplus in the exporting country.