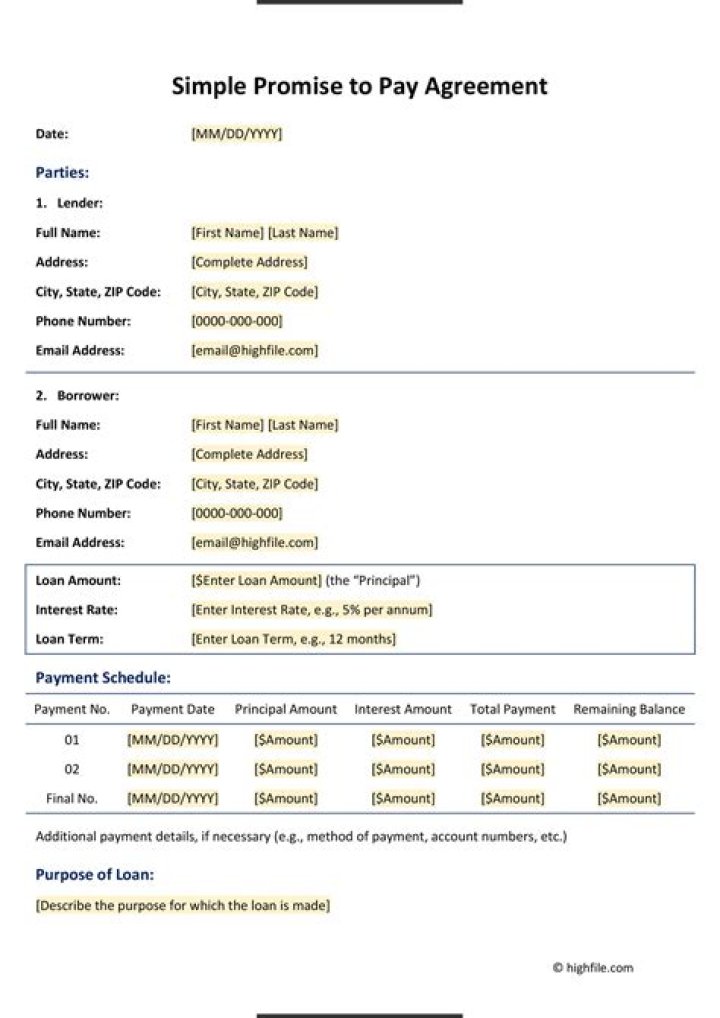

What is a signed promise to pay back a loan?

A promissory note is a written promise to pay within a specific time period. This type of document enforces a borrower’s promise to pay back a lender by a specified period of time, and both parties must sign the document. A promissory note is not the same as a contract.

What is a promise of payment?

It refers to the agreement between lender and borrower to pay for goods on a certain date.

How do you write a promise to pay note?

- Write the date of the writing of the promissory note at the top of the page.

- Write the amount of the note.

- Describe the note terms.

- Write the interest rate.

- State if the note is secured or unsecured.

- Include the names of both the lender and the borrower on the note, indicating which person is which.

Why do you need a promissory note and a loan agreement?

If the sum is not huge and the relationship is trustworthy, it is preferred to go with a promissory note to avoid potential legal issues. However, if the sum of money is huge and the relationship is not entirely trustable, make sure to use a secured loan agreement to ensure your money is safe with the borrower.

Can money be used as a promise to pay?

A promissory note is a financial instrument that contains a written promise by one party (the note’s issuer or maker) to pay another party (the note’s payee) a definite sum of money, either on demand or at a specified future date. In effect, promissory notes can enable anyone to be a lender.

What happens if you don’t pay a promise to pay?

Missing a Promise to Pay Agreement payment can be dangerous for the borrower. Many notes have acceleration clause; miss one payment, and the entire amount is due immediately. If you object to such a cause, don’t hold your peace while the deal is being done. Some deals call for penalties and fees for missed payments.

How does a promise to pay loan work?

The federal government regulates promise to pay loan agreements under the Truth in Lending Act. Lenders must provide borrowers with a statement that explains the cost of the loan, when a lender can assess charges, such as late fees, beyond the interest charges and what rights the borrower has.

What do you call a promise to pay letter?

A “Promise to Pay Letter” is a promise to pay a debt that is put in writing. These documents may also be known as a loan note or a loan agreement and is sometimes called an I.O.U. In most cases, the promise to play letter will be prepared by a loan officer at a bank or lender, but it can also be prepared by a lawyer.

What makes a person unlikely to pay back a loan?

Now, let’s consider language that suggests someone is unlikely to pay their loans. Generally, if someone tells you he will pay you back, he will not pay you back. The more assertive the promise, the more likely he will break it. If someone writes “I promise I will pay back, so help me God,” he is among the least likely to pay you back.

What happens when you pay back a promissory note?

The borrower should pay back the borrowed money on-time and in accordance with the note. If not, fees may be applied to the overall balance. Once all the money has been fully paid back to the lender a Loan Release Form is created and issued to the borrower relieving them from any liability from the note.