What is a fully insured policy?

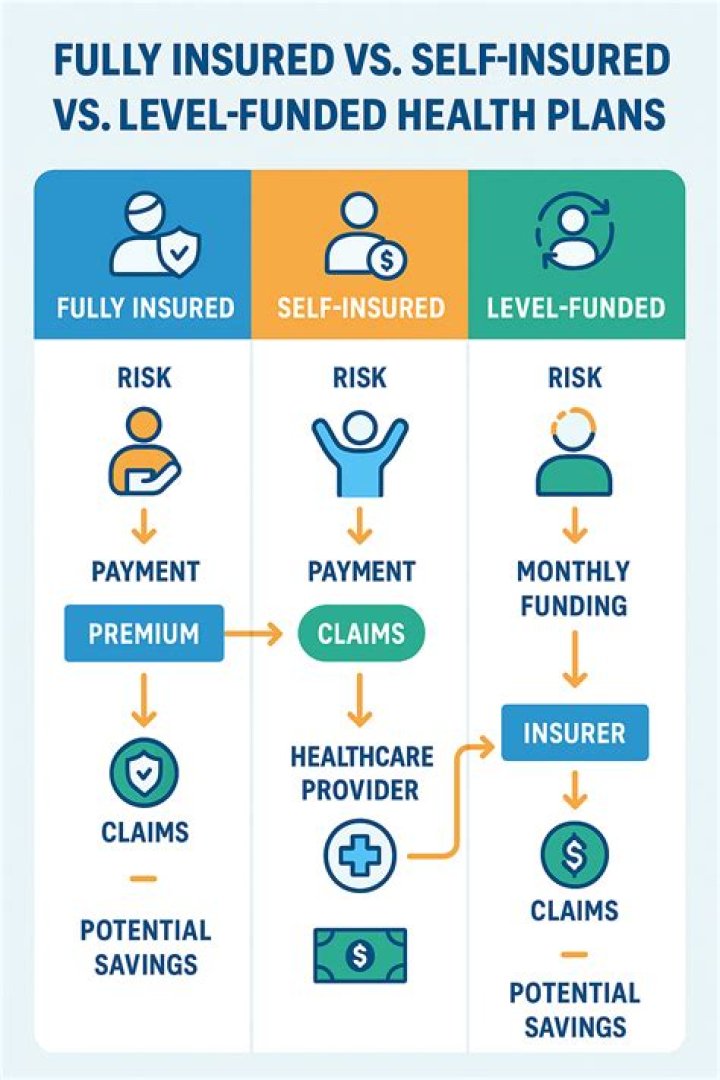

A fully insured plan is considered the more traditional way to structure and operate an employer-sponsored health plan. A company pays a premium to the insurance carrier, and premium rates are fixed for the year, based on the total number of employees enrolled monthly in the plan.

What is the difference between fully insured and self-insured?

Fully-insured health plans are what most people are familiar with—a traditional group health plan from an insurance carrier. Self-insured plans are funded and managed by an employer, often in an effort to reduce premium costs.

What is the difference between level funded and fully insured?

A fully insured plan removes most risk from the employer and employees, but the guaranteed cost of the plan is higher. Level-funding attempts to combine the best of both worlds, but is really only viable for a narrow segment of employers.

What does it mean for a company to be self-insured?

Being self-insured means that rather than paying an insurance company to pay medical, dental and vision claims, we pay the claims ourselves, using a third-party administrator to process the claims on our behalf.

Is PPO fully insured?

PPO, which stands for Preferred Provider Organization, is defined as a type of managed care health insurance plan that provides maximum benefits if you visit an in-network physician or provider, but still provides some coverage for out-of-network providers.

How does self-insurance work?

In a self-insurance arrangement, the employer takes on the risk of providing health insurance coverage for their employees. This is in contrast to a traditional arrangement where the employer/employee pays premiums (the monthly bill) to an insurance company, who then is responsible for paying all the eligible claims.

How can I tell if my employer is self-insured?

How can you know if your plan is self-insured? Because many employers use a third party administrator, such as an insurance company, to handle claims, you may not necessarily know if your plan is self-insured. To find out, contact your employee benefits administrator in your employer’s human resources department.

Is minimum premium fully insured?

Technically, minimum premium is a fully insured arrangement. Like level-funding, it captures 70% to 80% of the savings attributable to pure self-funding. Operationally, a minimum premium is remitted monthly to the insurer to pay the plan’s fixed expenses (e.g., claim administration, risk charges, etc.).

What does level funded mean in insurance?

With a level-funded plan, an employer pays a health carrier the same monthly amount to cover the estimated cost for expected claims, the premium for stop-loss insurance that covers health care costs over a set dollar amount, and plan administration costs.

What does a fully insured health plan mean?

Definition – What does Fully Insured Health Plan mean? A fully insured health plan is a health insurance plan in which an employer pays a specific premium amount to an insurance company to get coverage for a specific number of employees.

What’s the difference between fully insured and self insured insurance?

As always, insurance is a balance between costs and risks. A fully insured plan removes most risk from the employer and employees, but the guaranteed cost of the plan is higher. A self-insured plan leaves most of the risk with the employer, but also has the greatest chance for savings.

What is a partially self insured health plan?

A Partially Self-Insured Health Plan, with an Integrated HRA. One variation of a partially self-insured health plan is to raise the deductible on the group health insurance plan and self-insure the difference with an integrated Health Reimbursement Arrangement (HRA).

What’s the difference between level funding and fully insured?

With some level-funding providers offering their services to companies down to 10 full-time employees, these plans obviously can’t operate under the kind of risk possible with a larger company; the stop-loss coverage comes into play at a much lower threshold, protecting the company from unforeseen huge claims.