What happens to your PMI when you refinance?

The short answer: yes, private mortgage insurance (PMI) can be removed when you refinance. In most cases, PMI is cancelled automatically once the homeowner has reached 22% equity in the home – which is the same thing as “78% loan-to-value ratio (LTV).” You’ll see both terms used, so don’t be confused.

Will refinancing get rid of my PMI?

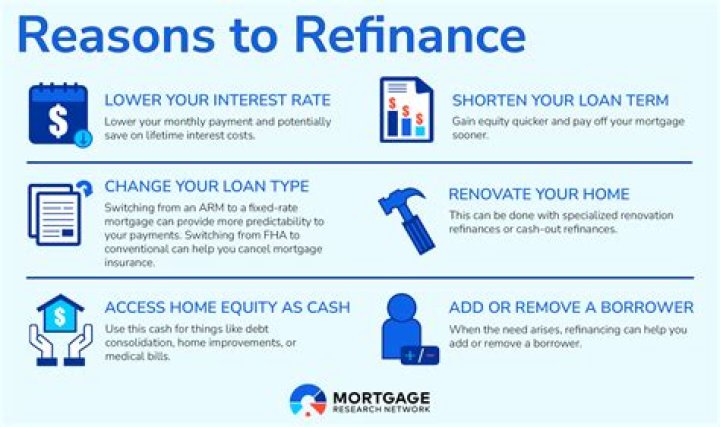

Besides getting a lower rate, refinancing might also let you get rid of PMI if the new loan balance will be less than 80% of the home’s value. But refinancing will require paying closing costs, which can include myriad fees. You’ll want to make sure refinancing won’t cost you more than you’ll save.

How do I avoid paying PMI when refinancing?

You can avoid PMI by simultaneously taking out a first and second mortgage on the home so that no one loan constitutes more than 80% of its cost. You can opt for lender-paid mortgage insurance (LMPI), though this often increases the interest rate on your mortgage.

Can your PMI increase?

Like principal and interest, private mortgage insurance premiums generally don’t change after your loan closes. That leaves home insurance premiums. Providers do increase them from time to time, however there are steps you can take to reduce this cost.

Can you get rid of PMI with a mortgage refinance?

“The interest rate [on non-conforming loan products] may be slightly higher than on a conventional loan,” Stockwell says. “But the elimination of mortgage insurance payments ends up reducing your total monthly mortgage payment.” A no-PMI refinance can yield big savings, depending on your current rate and loan balance. Take a look at one example:

What does PMI stand for in mortgage insurance?

What is PMI, or private mortgage insurance? PMI is a type of mortgage insurance that protects the lender in case you default on your mortgage. Homebuyers who use a conventional mortgage with a down payment of less than 20 percent usually are required to get private mortgage insurance.

Do you have to have PMI with a conventional mortgage?

Homebuyers who use a conventional mortgage with a down payment of less than 20 percent are usually required to get private mortgage insurance, or PMI. This is an added annual cost — about .03 to 1.5 percent of your mortgage. PMI doesn’t apply to all mortgages with down payments below 20 percent.

When is the best time to stop PMI payments?

When mortgage rates are low, as they are now, you might consider refinancing your mortgage to save on interest costs or reduce your monthly payments. At the same time, refinancing might enable you to eliminate PMI if your new mortgage balance is below 80 percent of the home value. It’s a double dose of savings.