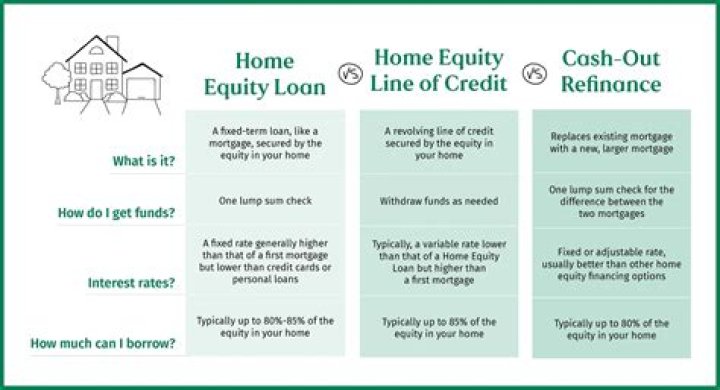

What happens to your Equity when you refinance your home?

If you do a “cash-out” refinance, however, your equity will drop. Equity is the market value of your property minus the outstanding loan amount. If your home is worth $200,000, and you have $150,000 of principal left to pay on the mortgage, your equity is $50,000.

Is it better to refinance or sell your home?

If you’ve spent years paying the mortgage, you’ve worked hard to build up equity, which provides a cushion during lean financial times and, ultimately, a profit if you decide to sell the home. However, a refinance can actually raise equity, under the right circumstances.

When is it the right time to refinance your home?

If you bought a home within the last five to seven years and you’ve built up equity, you might be thinking about refinancing. A refinancecan lower your payments and save you money on interest, but it’s not always the right move. In fact, these three mistakes could end up costing you in the long run.

What happens when you lose equity in Your House?

If you stay in your home long enough, you may see that the equity fluctuates. You can lose equity in a house and later regain it. In certain markets, it can take a long time for equity to make a rebound once it is lost. In other markets, equity can quickly rebound.

Can you refinance a HELOC with a cash out loan?

By refinancing your HELOC with a cash out refinance, you can get a single loan to pay off both your mortgage and your HELOC. You may be able to lock in a fixed interest rate and reduce your monthly payments. Can leave you with excess money, depending on your home’s value.

What can you do with the cash back from a refinance?

If you have the equity, you can use a cash-back refinance to get money for debt consolidation, remodeling, paying for college or just about anything else. Furthermore, pulling money out of your house is tax-free, and you frequently can write off the interest you pay on the loan.

How do you modify a home equity line of credit?

With a loan modification, you simply contact your lender and request an adjustment your loan by extending its terms or reducing its interest rate so that you can better afford the monthly payments.