What do banks use the interest they collect for?

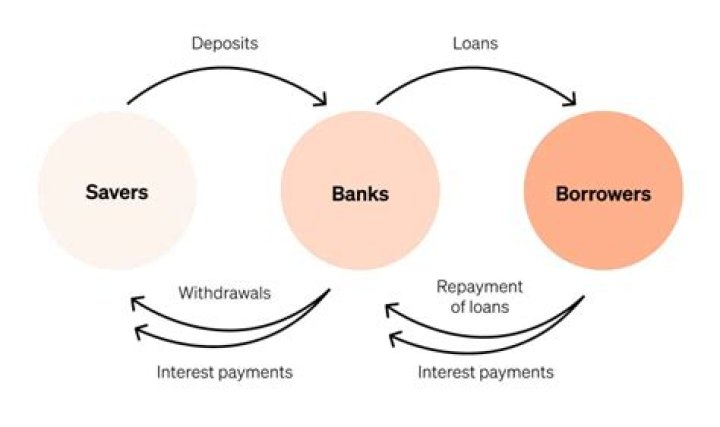

It all ties back to the fundamental way banks make money: Banks use depositors’ money to make loans. The amount of interest the banks collect on the loans is greater than the amount of interest they pay to customers with savings accounts—and the difference is the banks’ profit.

How do bank charge interest on loans?

As you repay the loan over time, a portion of each payment goes toward the amount you borrowed (which is the principal) and another portion goes toward interest costs. The loan interest charged is determined by things like your credit history, income, loan amount, loan terms and current amount of debt.

What happens when the interest rates on bank loans are high?

When interest rates are high, bank loans cost more. People and businesses borrow less and save more. Demand falls and companies sell less. The economy shrinks.

How is interest debited on a business loan?

Interest debited by bank directly:- Normally, business firm maintains the current account with the bank from whom it takes loans. The bank automatically debits the account of firm with the amount of interest on a particular date as agreed by both the parties.

Where does interest go on a bank loan?

Bank interest is a financial expenses. Therefore, it is indirect expenses and is shown in expenses side of profit and loss account. Accounting Treatment of Bank Interest Interest debited by bank directly:- Normally, business firm maintains the current account with the bank from whom it takes loans.

Which is the best interest rate to get from a bank?

As mentioned above, a bank’s prime rate—the rate banks charge to their most credit-worthy customers—is the best rate they offer and assumes a very high likelihood of the loan being paid back in full and on time. But as any consumer who has tried to take out a loan knows, a number of other factors come into play.

When do banks raise interest rates on loans?

When demand is low, such as during an economic recession, like the Great Recession, which officially lasted between 2007 and 2009, banks can increase deposit interest rates to encourage customers to lend, or lower loan rates to incentivize customers to borrow. Local market considerations are also important.