How much can you borrow against your 403b?

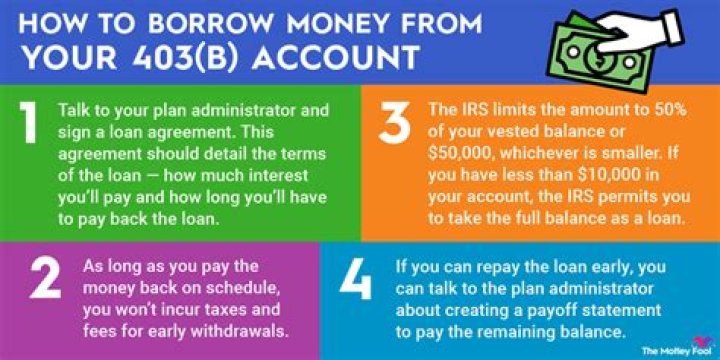

You can typically borrow up to half the vested amount in your retirement savings account, but no more than $50,000. If you already borrowed money within the past 12 months, then the balance of the loan will be subtracted from your allowable amount.

How do I borrow from my 403b retirement plan?

How do I borrow? One of the reasons 403(b) loans are popular is because the process to get one is simple and easy. If a loan is right for you, you simply call your plan provider and request the loan. As long as the plan permits, you could have the funds in your control within a few days.

What happens to a 403 B when you quit?

Your vested balance is the amount of your 403(b) that you get to keep if you quit. Your unvested balance will go back to your employer when you quit whether you leave your 403(b) there, transfer it to your new employer, or withdraw it.

Can you take a loan from your 403B plan?

If you need money from your 403 (b) plan, before you take a distribution, consider a 403 (b) plan loan. Taking a loan allows you to access the money in your plan without taking a permanent distribution, thus avoiding taxes and early withdrawal penalties. However, not all 403 (b) plans offer loans,…

What happens if I withdraw money from my 403B?

Ultimately, the interest you paid belongs to you. It doesn’t affect your credit score. Your 403 (b) loan is technically not a debt, so it doesn’t affect your credit score and your chances of getting approved for a traditional loan. You don’t have to return early withdrawal.

Can a 403 ( b ) plan be used for a down payment?

Your 403(b) plan is supposed to be your nest egg for retirement, but if you’re trying to come up with enough cash for your dream home, it can sure look tempting. If you’re not over 59 1/2, however, you might not be able to use your 403(b) plan for a mortgage down payment.

Are there limits on how much you can contribute to a 403B plan?

Thankfully these default repayments are not included in yearly contribution limits, however, the defaulted loan on a 403(b) or 457(b) account can prevent a participant from obtaining future loans from their retirement plan and is also included in the $50,000 maximum loan limit per year.