How long does a default affect mortgage?

A default (whether satisfied or not) will drop off your record after six years. Mortgage lenders prefer satisfied defaults because it shows them that, even though you previously failed to repay your debts, you’ve managed to pay it all back.

What happens if your 3 months late on your mortgage?

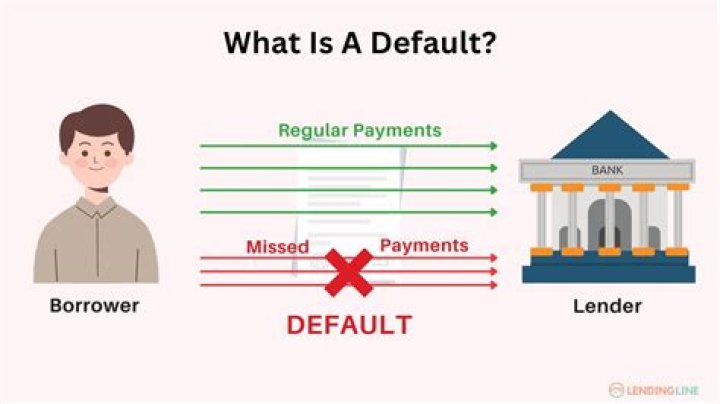

If you fail to pay and then miss another payment, things get more complicated. Late fees can be added, and your lender may report you to the credit bureaus, which will harm your credit score. Once you miss the second payment, you’re in default.

Does a default affect getting a mortgage?

Lenders are most interested in your recent credit activity, so if you have a default, even if it was registered in the past couple of years, you should be able to find a mortgage. If you have defaulted on a mortgage or other secured loan you are likely to be turned down whenever the default was registered.

What happens to my house if I default on my mortgage?

If you still fail to pay, the bank can take possession of the property, and ultimately sell the property under the terms of the mortgage agreement or by foreclosure. Any costs incurred by the bank when selling your home is added to the amount that you already owe.

Can You remortgage with a default on your credit file?

Yes, it can still be possible to remortgage with defaults on your credit file. As with other types of mortgage applications, it will all depend on the date the default was registered, the amount and if there are any other forms of bad credit on your credit file.

Is it possible to default on a secured loan?

Yes, they are. All lenders will consider secured loan or mortgage payment defaults to be very serious and weigh them accordingly when making a decision. However, some lenders are more relaxed about, for example, missed payments on mail order accounts or mobile phone contracts.

Why did my lender refuse to approve my mortgage?

Defaults on a credit file are one of the most common reasons for the refusal of a mortgage by many lenders, especially on the high street where generally only applicants with a clean credit history are approved.