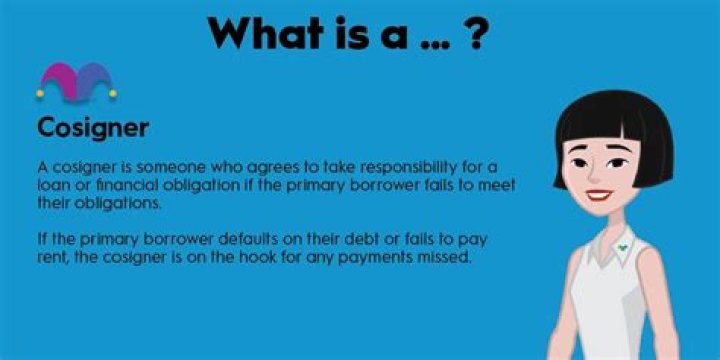

How is interest rate determined with a cosigner?

In a sense, a cosigner lends you her good credit history until you build — or rebuild — your own. The lender bases the interest rate for the loan on the cosigner’s credit score, so the interest rate is usually low if your cosigner has a solid payment history.

Is interest rate based on cosigner?

Your cosigner’s credit score – When you apply with a cosigner, their credit score is also factored in. They help lower your risk of defaulting on the loan, which can lead to a lower interest rate. The length of your loan term – Generally, the shorter your loan term, the lower your interest rate.

What’s the difference between a co signer and a co-borrower?

Both co-signers and co-borrowers share in the responsibility of taking out a loan. The key difference between a co-signer and a co-borrower is how much the loan benefits that party. A co-signer does not benefit; they are simply using their resources to help secure the loan for another person.

How does a cosigner affect your credit score?

Does Cosigning Affect Your Credit? When someone cosigns a loan for you, it ties the loan to their credit for its entire term. If you stop making loan payments and your cosigner is unable to take them over, you will both notice a drop in your credit scores.

When do you need a co signer for a car loan?

Lenders may ask you to find a co-signer if you seek a car loan but have a poor credit rating, inadequate income, or too little time on the job. Adding the co-signer’s good credit to your loan application can often help you to get the deal, but there can be situations where even a great co-signer isn’t enough.

Do you have to report a co-signer on your credit report?

From the perspective of your credit, whether or not you have a co-signer once you get the loan doesn’t matter. Since you’re still a signer on the loan, you’re responsible for it. This means that it should get reported on your credit report just like any other loan.