Does the amount of an installment loan affect credit score?

Late payments on anything (utilities, hospital bills, credit card bills, and installment loans) will reduce your credit score. Installment loans will not negatively affect your score as long as you are paying on time. Because of this, they forgive of large loan balances.

How many payments until you get a credit score?

About six months of on-time payments should help you get a decent credit score.

Should I pay off my installment loan?

Okay, so this question is actually pretty simple to answer: Yes, paying off your credit cards with an installment will almost certainly save you money in the long run. Here’s why: The standard term for a personal installment loan is anywhere between one and five years.

Does paying off an installment loan early hurt credit?

Even if you pay off the balance, the account stays open. And while paying off an installment loan early won’t hurt your credit, keeping it open for the loan’s full term and making all the payments on time is actually viewed positively by the scoring models and can help you credit score.

Can you pay back an installment loan early?

In summary, yes, if you have the right lender, you can pay off your installment loan early, and yes, we recommend it. It won’t hurt your credit score to do so, and there are many ways of building your credit that won’t cost you anything in monthly interest.

How does an installment loan affect my credit score?

Installment loans will not negatively affect your score as long as you are paying on time. That’s because when you first get a loan, credit agencies understand that the loan balance will be relatively high during the beginning of its lifetime.

How long do installment loans stay on your credit report?

If you had an installment loan and it’s been paid in full. The account will remain on your file for up to 10 years from the date of last activity (DLA). If you currently have an installment loan and have made late payments. Late payment history will generally remain on your file for up to 7 years.

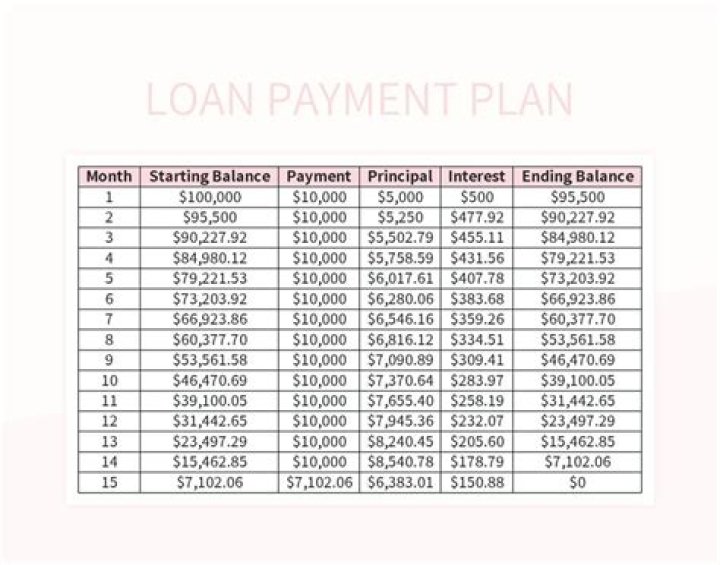

What do you need to know about installment loans?

Installment loans include any loan that is repaid with regularly scheduled payments or installments. If you are thinking about applying for an installment loan there are pros and cons to consider first. Here’s what you need to know before taking one out.

What happens when you pay off an installment loan?

An installment loan has a set number of scheduled payments spread over a predetermined period of time. When you pay off an installment loan, you’ve essentially fulfilled your part of the loan obligation. The balance is brought to $0, and the account is closed.