Does refinancing affect cosigner?

In the simplest language, refinancing a loan involves applying for a new loan with new terms which is used to pay off the old one. Then, you continue paying off your student loan under the new terms. This would eliminate your cosigner and end their responsibility for your loan.

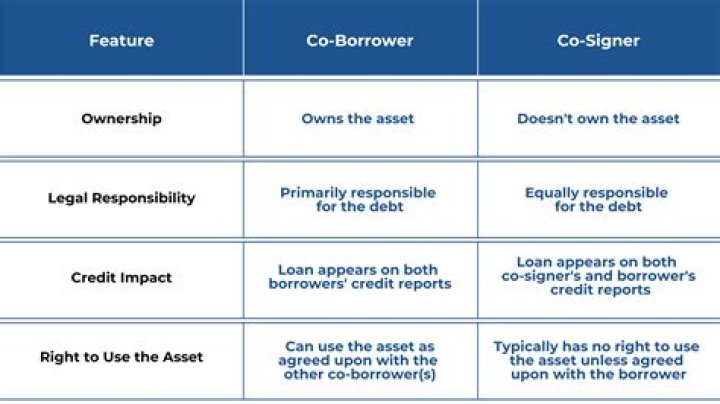

Does a cosigner own the property?

Generally speaking, a cosigner will be on the loan documents, such as the note and the mortgage and deed of trust. The cosigner will not be on title to the property, and will not sign the deed. The cosigner’s role is strictly on the loan application, and not with ownership of the property.

What are my rights as a cosigner on a mortgage?

Co-signers: Have no title or ownership in the property (house, car, etc.). Are legally obligated to repay the loan if the primary signer falls behind. Must have their income, assets, credit score and debt-to-income ratio considered in the loan application.

How do I remove a cosigner from a refinance?

To take the co-signer off the mortgage, the borrower must qualify for the refinance on his own financial merits. Qualification works exactly the same way as a purchase mortgage. Essentially, the lender will look at the borrower’s credit, income, assets and the value of the property itself.

Can a co-signer take over a mortgage?

A cosigner on a mortgage loan is almost always also a owner on the property. Most mortgage lenders will not make a mortgage loan to two borrowers if only one has a vested interest on the property deed. However, if managed correctly, it is still possible for a cosigner to take over a mortgage loan.

Can a co signer increase your mortgage payment?

The amount that your monthly mortgage payment may increase because you have a co-signer on the loan depends on numerous factors. The co-signer’s income and debt burden is factored into the equation with your income and debts. Conventional mortgage lenders may not allow all of a co-signer’s income.

What happens when a cosigner is taken off a mortgage?

If a different lender will be used, remortgaging will need to happen, in which a whole new loan will need to be obtained to pay off the existing mortgage. At that time, the new lender would then take over the loan and it would work as any other type of mortgage between the lender and the borrower.

What to know before cosigning a mortgage for your child?

A cosigner must have stable income, a low debt-to-income ratio, and good credit in order to help qualify for a mortgage loan. Krop says that financial advantages for a cosigner don’t exist. But, if it’s for your adult child, you are providing the opportunity for them to own a home when no one else would give them the chance.

Can a lender tack on income to a cosigner?

No lender — regardless of the type of mortgage — just tacks on the cosigner’s income to yours. If you want your co-signer to deliver a larger mortgage, she has to undergo a DTI review just like you.