Can you lose your home with a reverse mortgage?

The answer is yes, you can lose your home with a reverse mortgage. However, there are only specific situations where this may occur: You no longer live in your home as your primary residence. You move or sell your home.

Who owns your house when you have a reverse mortgage?

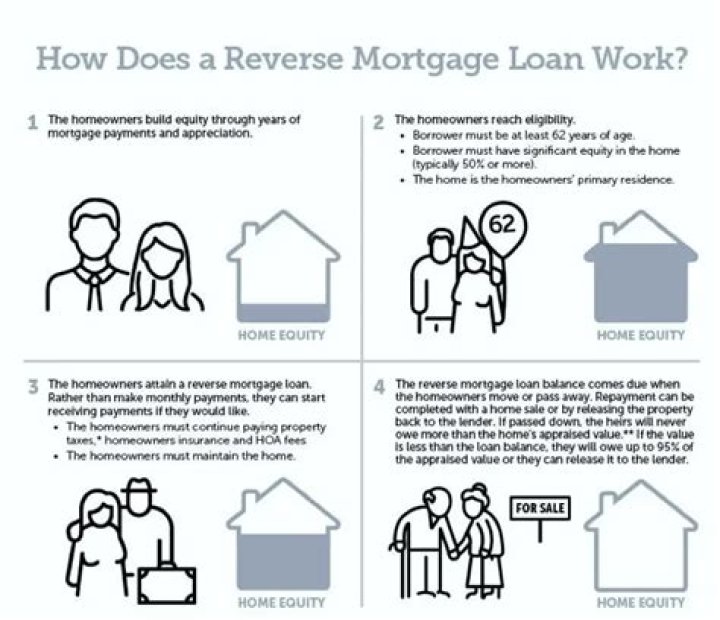

When you take out a reverse mortgage loan, the title to your home remains with you. Most reverse mortgages are Home Equity Conversion Mortgages (HECMs). The Federal Housing Administration (FHA), a part of the Department of Housing and Urban Development (HUD), insures HECMs.

What happens when reverse mortgage runs out?

What happens if my reverse mortgage loan balance grows larger than the value of my home? If you owe more than your home is worth, but sell your home for the appraised fair market value, the remaining balance will be paid by mortgage insurance. When the last remaining borrower passes away, the loan has to be repaid.

Why is credit pulled on a reverse mortgage?

Credit is only pulled to verify liens, other mortgages listed and or possible judgments. Shane is correct it is a negative ammortizing loan. On another note, I just want to add…In regards to “why not just take out a HELOC when you have good FICO scores”?

Do you have to have good credit to get a reverse mortgage?

Reverse mortgages do not take credit scores into consideration. However, there is a financial assessment portion of the underwriting. It would depend on other areas of your payment history (house payments, property taxes, home insurance, etc.).

How long does it take for your credit to recover from a reverse mortgage?

If they have a bunch of equity and decent credit and just need more of a short term type help, maybe some sort o HELOC type thing that they can then pay off as they can. Anyways, between the inquiry and the new credit line, they will likely see a small credit score drop. It should recover in 6 months or so. 09-21-2009 07:26 PM 09-21-2009 07:26 PM

What makes a person ineligible for a reverse mortgage?

Delinquent federal non-tax debt — If it is determined that a borrower has delinquent federal non-tax debt, the lender must verify it with a creditor agency. If the creditor agency verifies the debt is valid and delinquent, then the borrower is ineligible for a reverse mortgage until the delinquency is resolved.