Can I have two conventional loans?

This loan structure uses a conventional loan as the first mortgage (80% of the purchase price), a simultaneous second mortgage (10% of the purchase price), and a 10% homebuyer down payment. The combination of both loans can help you avoid PMI, because the lender considers the second loan as part of your down payment.

How can I avoid a jumbo loan?

How to Avoid a Jumbo Mortgage (And Its Jumbo Rate)

- Get a conforming mortgage and get a second mortgage along with it. This lets you enjoy the low rate on the $417,000; you’ll pay the higher rate only on the rest.

- Take out a super-conforming mortgage and a second trust.

- Get an adjustable-rate mortgage.

Are jumbo loan rates higher than conventional?

In fact, jumbo mortgage rates are often competitive and may be lower than conforming mortgage rates. It ultimately depends on the lender and the market conditions. But, if lenders are able to provide jumbo mortgages, they’ll usually keep their rates competitive. Interest rates aren’t only related to market conditions.

What is the conventional loan limit for 2021?

$548,250

For 2021, the Federal Housing Finance Agency raised the maximum conforming loan limit for a single-family property from $510,400 (in 2020) to $548,250. In high-cost areas, the ceiling for conforming mortgage limits is 150% of that limit, or $822,375 for 2021.

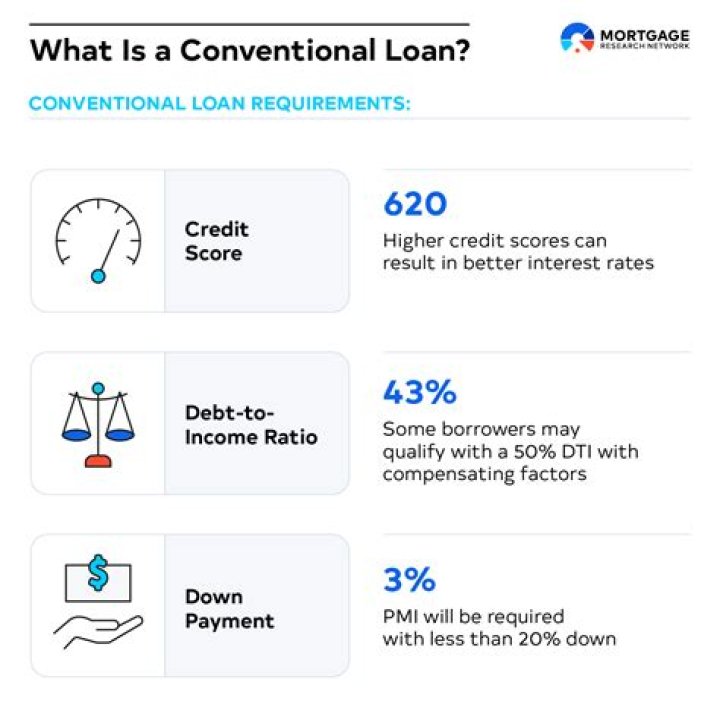

Is a conventional loan hard to get?

Even though a conventional loan is the most common mortgage, it is surprisingly difficult to get. Borrowers need to have a minimum credit score of about 640 in order to qualify—the highest minimum score of all mortgage products—and have a debt-to-income ratio of 43% or less.

What is considered a jumbo loan in 2020?

A jumbo loan (or jumbo mortgage) is a type of financing where the loan amount is higher than the conforming loan limits set by the Federal Housing Finance Agency (FHFA). The 2021 loan limit on conforming loans is $548,250 in most areas and $822,375 in high-cost areas.

What’s the difference between a jumbo loan and a conventional loan?

In the past, interest rates for jumbo loans were much higher than traditional mortgage rates. Although the gap has been closing, they are still slightly higher. Down payment requirements were also similarly structured—at one point reaching as high as 30%. But it is more common now to see jumbo loans requiring a down payment of about 10% to 15%.

What’s the difference between Jumbo and conforming mortgages?

Down payment: Whether conforming or jumbo, you need to make a down payment on your mortgage. Often, jumbo loans require larger down payments than conventional loans. It’s not uncommon for lenders to expect a minimum of 20% down payment for jumbo loans.

Can you take out a Jumbo home loan?

Some lenders will let you take out a jumbo mortgage. These are non-conforming mortgages used to finance homes over the FHFA loan limit. These mortgages are typically kept by the lender and are not guaranteed or insured, which makes them riskier. Every jumbo lender will have its own standards for making these loans.

What’s the maximum loan amount for a jumbo loan?

A jumbo home loan is a mortgage that exceeds the maximum conforming loan amount. A conventional mortgage must meet the loan limits spelled out by either Fannie Mae or Freddie Mac. For most areas, that’s $510,400 for 2020.