Can I deduct mortgage prepayment penalty?

Mortgage prepayment penalty. If you pay off your home mortgage early, you may have to pay a penalty. You can deduct that penalty as home mortgage interest provided the penalty isn’t for a specific service performed or cost incurred in connection with your mortgage loan.

Is a mortgage prepayment penalty considered interest?

In each case, the penalty is directly related to the amount borrowed under the financing agreement. The payment is not for any specific services, other than for the loan. For this reason, the prepayment penalties are deductible as interest to Taxpayer.

Can I deduct my closing costs on tax return?

Can you deduct these closing costs on your federal income taxes? In most cases, the answer is “no.” The only mortgage closing costs you can claim on your tax return for the tax year in which you buy a home are any points you pay to reduce your interest rate and the real estate taxes you might pay upfront.

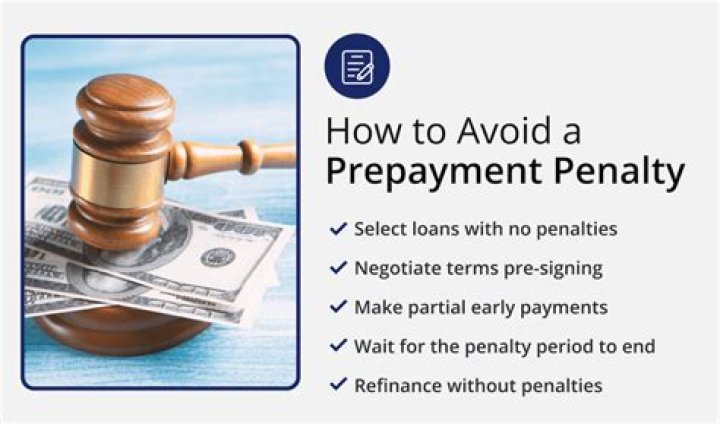

Is there a penalty for prepaying a home loan?

The prepayment penalty is limited to no more than 2% of the outstanding loan balance if you prepay during the first two years of the loan, or 1% if you prepay the loan during the third year. Some states set additional limits as well. Is the prepayment penalty tax deductible?

Can you deduct the prepayment penalty in one year?

To deduct the entire prepayment penalty in one year, you must pay the penalty in full. If you refinance and roll the penalty into your new loan, you can deduct the penalty over the life of the loan.

Can you deduct the prepayment penalty when you refinance?

If you refinance and roll the penalty into your new loan, you can deduct the penalty over the life of the loan. For borrowers who refinance but choose to pay the prepayment penalty at closing, the entire penalty is deductible.

Do you get a tax deduction for mortgage prepayment?

But at least you can deduct this penalty on your income taxes, something that can lessen, at least slightly, the financial sting. Lenders sometimes include prepayment penalties that kick in if you pay off your mortgage loan too early, usually within 3 to 5 years.