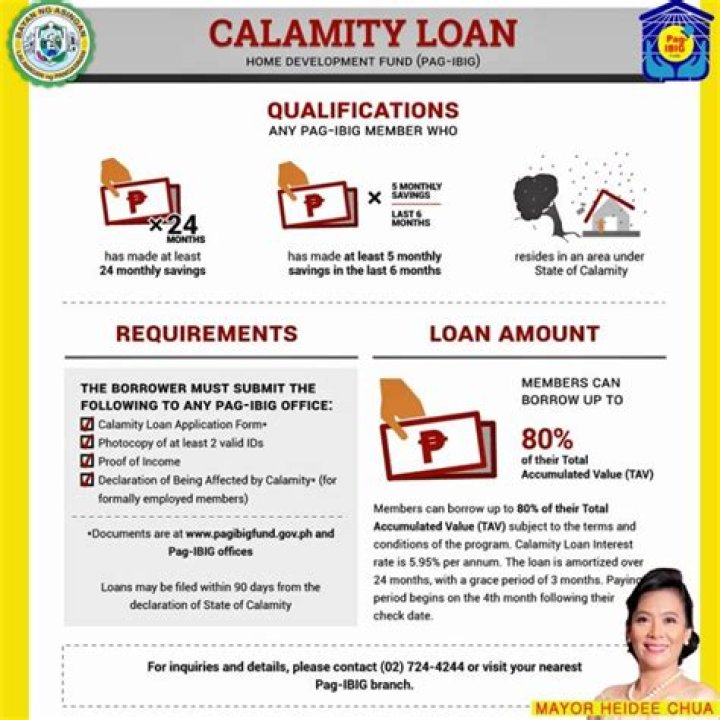

Can I avail PAG-IBIG calamity loan with existing loan?

A member can have an existing Pag-IBIG Fund MPL and still apply for Calamity Loan, as long as the member is updated with the payment of monthly contributions prior to the enhanced community quarantine done on 16 March 2020.

Can I have 2 loans in Pag-ibig?

YES. A qualified Pag-IBIG member who has an existing housing loan may avail himself of an additional housing loan for the following purposes: Purchased of lot / house and lot / condominium unit / townhouse / row house adjacent to the property mortgaged with the Fund.

When can I Reloan in Pag-ibig?

When can I renew my MPL? You may renew your MPL after paying an equivalent of six (6) monthly amortizations and upon satisfying the qualifications mentioned above. The outstanding balance of your existing loan shall be deducted from the loan proceeds of your new loan.

Is salary loan deducted to calamity loan?

Never miss a Moment If you wish to file for a salary loan application, may we inform that any outstanding short-term loan (e.g. calamity loan, salary loan) balance in the SSS records will be deducted to the current salary loan proceeds, subject to its existing guidelines.

How can I check my PAG IBIG contribution online?

How to Check Pag-Ibig Contribution Online in 5 Easy Steps

- Step 1: Visit the Pag ibig Website to check your contribution online.

- Step 2: Login in Virtual Pag Ibig with your username and password.

- Step 3: Go to Regular Savings and input the year you want to view your contribution.

How much can I loan in Pagibig?

Php6 million

The Pag-IBIG Fund Housing Loan allows you borrow up to Php6 million to purchase a residential lot, a house and lot or a condominium unit. You may also secure a loan for house construction, home improvement or renovation or even to refinance an existing housing loan.

How much is the maximum loanable amount in Pag ibig?

A qualified Pag-IBIG member shall be allowed to borrow an amount up to a maximum of Six Million Pesos (Php 6,000,000.00), which shall be based on the lowest of the following: The Member’s Actual Need, His Loan Entitlement Based On Capacity To Pay, The Loan-To-Appraisal Value Ratio.

Can I withdraw my Pag Ibig contribution?

You may withdraw your Pag-IBIG Regular Savings should any of the following occur: Membership maturity after 20 years, equivalent to 240 monthly contributions. Retirement at age 60 (optional) or 65 (mandatory) Separation from service due to health reasons.

Can a calamity loan be used for a multi purpose loan?

If you have an existing calamity loan, you can only avail of MPL (Multi-Purpose Loan) if you complete at least 6 monthly amortizations. Outstanding balance, interest, and penalties shall be deducted from the MPL. If you are looking for a loan renewal, there is a different set of requirements.

Can you get a Pag ibig calamity loan if you have an existing loan?

Therefore, you can still avail of the Pag-IBIG Calamity Loan even if you have an outstanding Multi-Purpose Loan (provided that the payments are updated and the loan is not in default) and vice versa. In the same way, the outstanding balance of one loan will not be deducted from the loan proceeds of another.

Can You avail an SSS calamity loan even if you had an?

I still have an existing SSS salary loan when I applied and got approved for my sss calamity loan (July 2020). However, I’m not sure if I can apply for a new sss salary loan (after I fully paid my first) while I still have an existing sss calamity loan.

Can a short term loan be used for a calamity?

In an event that there is an earthquake, flood or any other calamity, it is also possible that you can avail of the calamity loan. Similar to the requirements on how to avail of a short term loan, it is also applicable to this setup.