Are car loans recourse or nonrecourse?

Most automobile loans are recourse loans. If the borrower defaults, the lender can repossess the car and sell it at full market value. This amount may be less than the amount owed on the loan because vehicles depreciate significantly in their first couple of years.

Is Washington state a non-recourse state?

Home mortgages—though generally recourse—are non-recourse in 12 states: Alaska, Arizona, California, Connecticut, Idaho, Minnesota, North Carolina, North Dakota, Oregon, Texas, Utah and Washington.

Are SBA loans Non-recourse?

Limited personal guarantees require SBA Form 148L.

Are SBA loans recourse or nonrecourse?

SBA has no recourse (or will demand compensation or payment) against individuals, shareholders, members, or partners of an eligible recipient unless the ‘covered loan’ proceeds are used for unauthorized purposes (see above). There are no personal guarantee requirements and no collateral requirements for ‘covered loans.

What happens in a non recourse loan state?

Generally, in a non-recourse state, if a lender cannot recoup its loan from the sale or seizure of the asset used for collateral, then the relevant state law will limit the lender’s ability to collect from the borrower. In a non-recourse state, if you default on your home loan, the bank can only foreclose on the home.

What makes a car loan a recourse loan?

Most automobile loans are recourse loans. If the borrower defaults, the lender can repossess the car and sell it at full market value. This amount is much lower than the value of the loan because vehicles depreciate significantly after it’s driven off the lot.

Are there any states that have non recourse laws?

Each state implements “non-recourse” or “anti-deficiency” laws differently. As of this writing, the following states have some form of non-recourse or anti-deficiency law: Alaska, Arizona, California, Connecticut, Iowa, North Carolina, North Dakota, Minnesota, Montana, Oregon, and Washington.

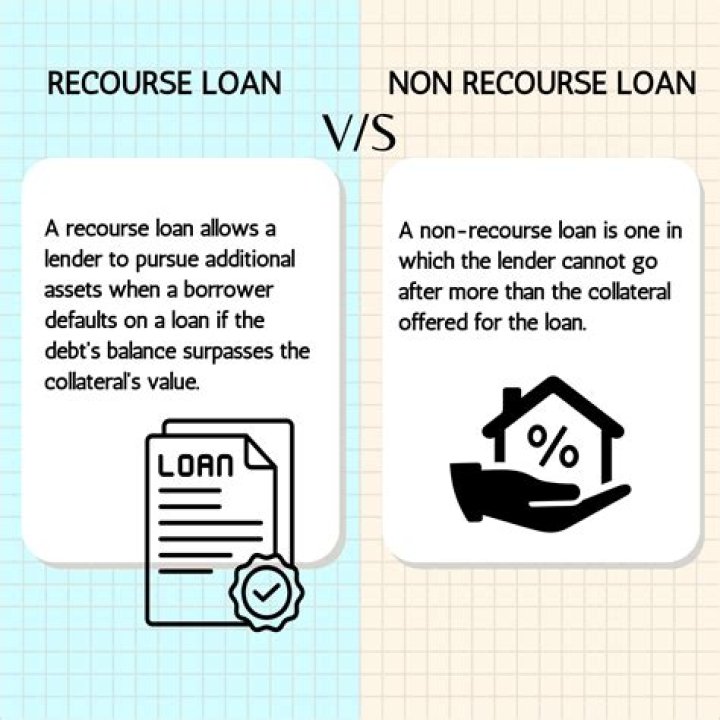

What is the collateral for a recourse loan?

In most cases, the collateral is the asset that was purchased by the loan. For example, in both recourse and non-recourse mortgages, the lender would be able to seize and sell the house to pay off the loan if the borrower defaults.